15 February 2023

Do the NextGenerationEU funds hold up to their promise to make Europe’s economies stronger and more resilient? Two years into the lifetime of the programme, this ECB Blog post assesses where governments stand and what risks there are for implementation.

NextGenerationEU (NGEU)[2] can really make a difference for European economies. ECB staff estimate that, if fully implemented, NGEU may increase the level of real gross domestic product (GDP) in the euro area – on which this blog focuses – by up to 1.5% by 2026.[3] This makes quite a difference as it will lift the growth prospects further on.

The potential boost comes via two primary channels:

- Money for investment – euro area governments plan to draw more than €417 billion in EU grants and loans from the Recovery and Resilience Facility (RRF) – the cornerstone of NGEU – in the period 2021-2026.[4] Around 80% of these resources are intended to fund investment projects.

- Incentives for better economic structures – the RRF links its disbursements to qualitative milestones and quantitative targets, of which 1,620 are related to structural reforms in euro area countries.

Already today, the implementation of the national Recovery and Resilience Plans (RRPs) is producing material benefits to the European citizens. These include savings in energy consumption, additional capacity for renewable energy, promoting digital products and services, modernisation of the public administration, as well as the creation of new infrastructure for transport, healthcare, and education.

NGEU’s impact is expected to be larger in the main beneficiary countries, such as Italy and Spain. All European countries are expected to benefit through positive trade and confidence effects, greater economic resilience, increased convergence across countries and, very importantly, a significant boost to the green transition and digital transformation.[5]

And yet, NGEU can only reach its full potential if all national reform and investment plans are implemented in a timely, efficient, and effective way. Hence the question: two years after its adoption, is NGEU delivering on its roadmap?

Timely implementation is at risk

The RRF disbursements to euro area countries have so far reached €130 billion. This amounts to more than 30% of the total envelope expected to be requested by these countries in the period 2021-2026. In 2021-2022, 14 euro area members made 22 payment requests under the RRF, of which 12 were approved.[6] While by the end of 2022 only 7% of milestones and targets had been completed in the whole EU, this share reached 22% in Spain and France, and 18% in Italy.

While this shows that NGEU is making good progress, there are also some delays. Why is this?

First, several euro area countries have postponed their disbursement requests.[7] In some cases the required structural reforms were delayed, and as these are preconditions for paying out the funds, there has been a knock-on effect on the schedule for payments.[8]

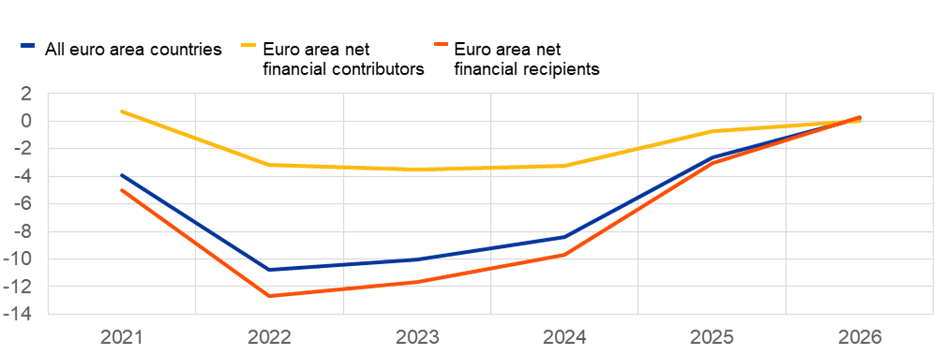

Second, some countries have postponed their investments funded by the RRF. This is illustrated in Chart 1, which reports aggregate estimates[9] of the annual deviation of NGEU-funded government expenditure compared with the initial Recovery and Resilience Plans (RRPs). Negative values indicate underspending. The chart shows that in 2021 and 2022 the NGEU expenditure plans were not executed completely. Forecasts for 2023-2026 indicate that Member States plan to catch up on investment objectives in the remaining years of the NGEU, notably in 2025.

Chart 1

Revisions in NGEU-funded government expenditure in the euro area countries in December 2022, compared with their original Recovery and Resilience Plans (cumulative)

Cumulative change in the share of total funds allocated

Percentage points

Source: Estimates of the Working Group on Public Finance of the European System of Central Banks.

Notes: The baseline against which revisions are measured are the original Recovery and Resilience Plans (RRPs) as approved in 2021 for most countries. Where RRPs do not specify a time profile of expenditure, expert judgement was applied. Luxembourg is the only country that did not change its NGEU expenditure plans. The euro area net financial contributors are Belgium, Germany, Estonia, Ireland, France, Luxembourg, Malta, the Netherlands, Austria, and Finland. The euro area net financial recipients are Croatia, Cyprus, Spain, Greece, Italy, Latvia, Lithuania, Portugal, Slovenia, and Slovakia.

Given the large amounts foreseen, the delays in the past two years will test the countries’ capacity to fully absorb the RRF funds by the end of the programme in 2026.

Two main categories of NGEU implementation risks are detected in virtually all euro area countries. First, the energy crisis and higher inflation have been raising new challenges. Procurement contracts and public tenders often need to be revised due to higher inflation. The persistence of supply bottlenecks – that is, problems to access the necessary materials, equipment, and skilled workers – has also created hurdles.[10] The second key driver is limitations in administrative capacity and political hurdles,[11] such as:

- deficiencies in the coordination between central/federal and local authorities[12];

- inadequate technical expertise in the public administration;

- too complex administrative practices and insufficient fast track procedures when needed;

- insufficient quality of monitoring and controls, auditing, and impact assessment; and

- low political consensus on some critical measure.

Policymakers need to step up their efforts to address these shortfalls. The quality and capacity of public administration, including public financial management, is itself a key area for reform projects in the RRPs of Member States with lower administrative capacity.

Past country performances in the absorption of EU funds offer a cautionary tale. By the end of 2020, no more than 60% of EU funds under the 2014-2020 Multiannual Financial Framework had been absorbed in the four biggest euro area countries. In the previous period 2007-2013, a grace period of another three years was required before a share of funds closer to 100% could be absorbed (Chart 2, dotted lines). The question, therefore, arises whether the six-year horizon of NGEU will be sufficient to absorb much bigger[13] – and by now to some extent already backloaded – EU funds along the foreseen path shown in Chart 2 (see solid lines).

It is, therefore, too early to draw any firm conclusions on the implementation of NGEU. To be sure, 2023 will be a crucial year to scrutinise on both fronts of investment and reforms.

Chart 2

Projected cumulative absorption rates of Recovery and Resilience Facility (RRF) funding compared with realised absorption rates of past Multiannual Financial Frameworks (MFF)

x-axis: year of programme; y-axis: absorption as cumulated percentage of total envelope

Sources: European Commission and estimates of the Working Group on Public Finance of the European System of Central Banks. For France, cash pay-outs under RRF according to Coeuré report (2021).

Notes: The solid lines refer to the foreseen absorption of RRF funds in Germany (DE), France (FR), Italy (IT) and Spain (ES) over the RRF period (2021-2026). The dotted lines refer to the actual absorption by these four countries of past EU resources made available under the EU’s Multiannual Financial Framework (MFF). The absorption rate is the amount paid to a Member State as a percentage of the total EU budget made available to that country. Year 1 is the first year of the respective programme, i.e., 2007 for the 2007-13 MFF, 2014 for the 2014-20 MFF, and 2021 for the RRF. Pre-financing under the RRF is included in Year 1. The absorption rate of the 2007-13 MFF (black dotted line) is shown as average of the four countries and includes the European Regional Development Fund (ERDF), the Cohesion Fund (CF) and the European Social Fund (ESF), while the 2014-20 MFF includes only the ERDF and the CF. Data under the 2014-20 MFF are provisional for the year 2021 (year 8 in the chart).

NGEU as a test for further EU integration

A successful NGEU may reinforce the case for a permanent central fiscal capacity for investment in European public goods such as climate change mitigation, energy autonomy, security, and the digital transformation.[14] A European fiscal capacity, if properly designed, could also play a role in enhancing macroeconomic stabilisation and convergence in the euro area in the longer run.[15]

By linking EU funding to the implementation of nationally owned structural reforms, NGEU is also pioneering an innovative, more integrated approach to EU economic governance. This approach recognises that reforms, investment, and fiscal sustainability are mutually reinforcing and should be better incorporated in fiscal and macro-structural surveillance.[16]

NGEU is a once-in-a-generation opportunity for Europe in a double meaning. Only a successful and timely implementation will keep the promise of making our economies stronger and more resilient. And at the same time and if successful, NGEU could become a role model for further economic integration in the European Union. It is an opportunity Europe should not miss.

Subscribe to the ECB blogAcknowledgements: based on evidence from the ESCB Working Group on Public Finance, with inputs and comments from O. Arce, C. Checherita-Westphal, C. Kamps, D. Kapp, N. Leiner-Killinger, B. Lichtenauer, C. Nickel, M. Rodriguez Vives, P. Rother, R. Setzer, A. Sterescu, and A. Trzcinska.

NGEU is a temporary funding instrument of the European Union that can mobilise up to €807 billion in grants and loans, subject to the completion of investments and structural reforms measures

See Bańkowski, K., Bouabdallah, O., Domingues Semeano, J., Dorrucci, E., Freier, M., Jacquinot, P., Modery, W., Rodríguez-Vives, M., Valenta, V., and Zorell, N. (2022), "The economic impact of NextGenerationEU: a euro area perspective", European Central Bank, Occasional Paper Series No. 291 (April). These estimates were finalised before the recent surge in inflation, which implies lower investment in real terms. The positive impact of investment on long-run growth may therefore be somewhat overestimated. On the other hand, additional positive effects not included in these estimates may stem from the crowding-in of private investment, cf. De Santis, R., Freier, M. and Vinci, F. (2022), “Business investment and the NGEU – crowding in or crowding out?”, ECB Economic Bulletin, Issue 5/2022, Article 1, Box 3.

Out of a total RRF envelop of €723.8 billion for the whole European Union, the euro area countries have requested their whole RRF grant entitlement. However, only Italy, Greece (in full), Cyprus, Portugal and Slovenia (in part) are making use of the loan facility, at least for the time being. Countries with borrowing costs below the EU average have not requested loans thus far.

The green transition will receive further support from the more recent REPowerEU initiative, which, inter alia, aims at gaining greater energy autonomy and unfreezing the envelope of unused NGEU loans (up to €225 billion for the whole EU).

These 12 payment requests exclude pre-financing payments by the EU Commission; all of them have been made in the form of grants, and 4 have also included loan payments. According to the Commission’s Recovery and Resilience Scoreboard, 14 euro area members – Austria, Croatia (which has become the twentieth euro area member on 1 January 2023), Cyprus, Spain, France, Greece, Italy, Latvia, Lithuania, Luxembourg, Malta, Portugal, Slovenia and Slovakia – have submitted payment requests thus far. The other euro area countries are in the pipeline.

In the original plans, the RRF instalments were in most Member States expected to be either frontloaded or spread relatively evenly over the 2021-2026 RRF programme period.

Such rescheduling is not necessarily bad news, as it points to the seriousness with which Member States are implementing, under the scrutiny of the Commission, the reform commitments taken in their RRPs. The RRF being a “performance-based instrument”, disbursements are not the reflection of costs, but the result of completion of the underlying milestones and targets.

These estimates have been prepared by the Working Group on Public Finance of the European System of Central Banks.

For instance, the insufficient availability of raw materials has delayed some public expenditure projects aimed at improving energy efficiency in public and residential buildings. Similarly, labour shortages have been holding up the implementation of public infrastructure projects.

While it is relatively easy to implement previously budgeted projects (estimated at about one fourth of total RRF-funded investment), it may take more time to effectively implement new investments, for instance because of backlogs in the completion of feasibility studies, complications in the procurement process, or risks of resource misuse that need to be counteracted.

In some cases, this may take the form of excessive centralisation of decisions at central government level, which impedes the adaptation of the projects to the specific needs of each territory. In other cases, there may be insufficient technical assistance to less developed regions and small municipalities.

When considering the RRF together with the other NGEU components (ReactEU, Just Transition Fund, Rural Development, InvestEU, Horizon Europe, and RescEU) and the new REPowerEU chapter, NGEU makes the funding available to euro area countries almost four time bigger than the funding under the regular 2021-2027 EU Multiannual Financial Framework (around €200 billion).

Such a proposal is outlined in Panetta, F. (2022), “Investing in Europe’s future: The case for a rethink”, Istituto per gli Studi di Politica Internazionale (ISPI), November (see here).

This is advocated by the ECB Governing Council in its statement on EU economic governance of December 2021.

The Commission has reflected this approach in its recent Communication on EU economic governance, which proposes the adoption of medium-term fiscal-structural plans combining reforms and investment with prudent national fiscal strategies. See European Commission (2022), “Communication on orientations for a reform of the EU economic governance framework”, 11 November.